WRITTEN BY: Siobhan Simpson | Head of SA Unit Trusts | Ninety One

For more than a decade, passive investing has been one of the defining trends in global asset management. Low costs, simplicity, and strong performance have made index-tracking strategies increasingly popular with investors.

Yet beneath the surface lies a more nuanced story, characterised by concentration risk and the potential opportunity cost of underexposure to emerging structural growth areas.

These risks tend to become more apparent as markets rotate from one cycle to the next, leaving investors who are heavily exposed to index-tracking strategies with insufficient depth to fully achieve their intended investment outcomes. In environments such as these, active management offers an advantage: the ability to allocate selectively, manage risk more effectively, and capture opportunities as they arise.

Defined by a narrow group of winners

Passive strategies typically track indices that are weighted according to market capitalisation. In simple terms, the larger a company becomes, the larger its representation in the index. As companies perform well and their share prices rise, their weight within the index automatically increases.

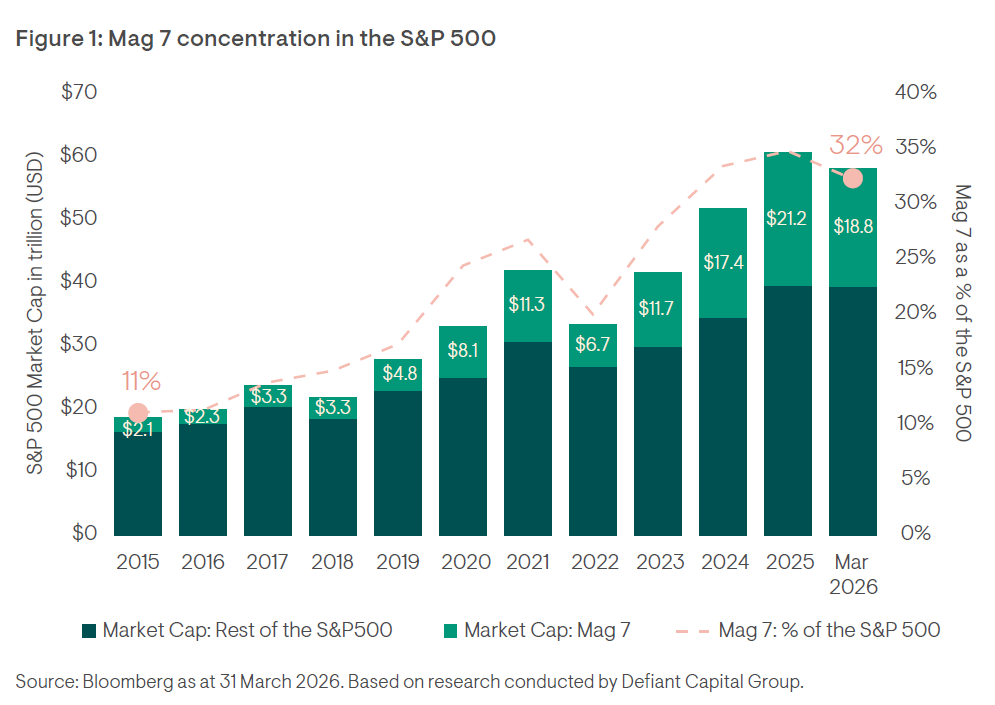

Evidence of this can be seen in the US, where a relatively small number of large technology companies, often referred to as the Magnificent 7 (Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla), have driven a significant share of overall market performance. While their dominance reflects genuine innovation, particularly in AI and digital infrastructure, it has also created an environment in which index performance is closely tied to the fortunes of a handful of companies and themes.

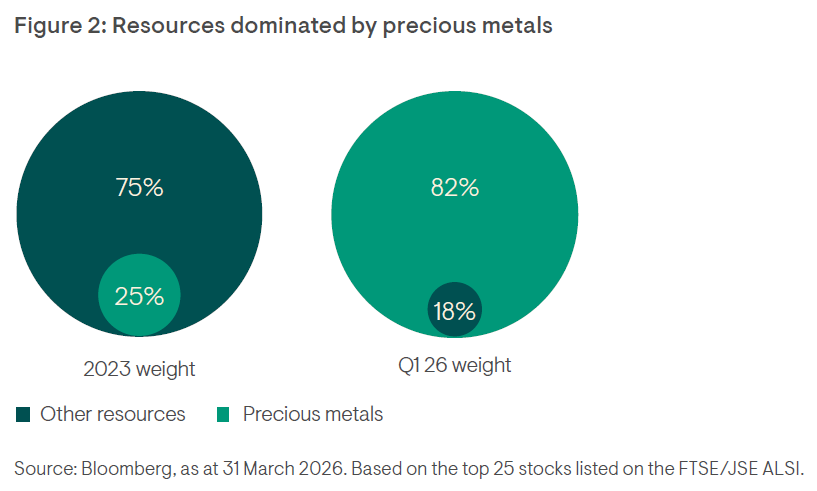

A similar pattern has emerged in South Africa, where after several years of relatively subdued performance, the domestic equity market has staged a notable recovery. But much of this rebound has been concentrated in specific sectors, particularly precious metals companies, which have benefited from stronger commodity prices.

When looking at the top 25 companies within the FTSE/JSE ALSI (which make up roughly 75% of the index), the change in composition over the past two years shows resources companies increasing from 22.0% to 31.3%. While this gain in isolation may not raise concerns about concentration risk, a closer inspection of its composition might.

Of the total 31.3%, approximately 25.6% is derived from just seven precious metals companies. Gold Fields and AngloGold Ashanti are perhaps the biggest beneficiaries of this change, collectively accounting for 14.6% of the entire index as at the end of March 2026, up from just 5.5% as at the end of 2023.

Finding opportunities beyond the index

The global economy has undergone a period of meaningful structural change, driven by technological disruption, geopolitical realignment, and shifting supply chains.

Advances in areas such as artificial intelligence and automation have reshaped industries and redefined competitive advantages. At the same time, changing geopolitical dynamics have prompted countries and companies to rethink trade relationships, energy security, and strategic priorities. Supply chains, meanwhile, have become more regional and resilient, rather than simply optimised for cost. Together, these forces have reshaped market leadership into what we see today, but perhaps more importantly, they are creating opportunities for new winners and investment themes to emerge.

For investors, this shift matters. Passive strategies tend to be anchored to past winners, with increased exposure to established leaders, while missing emerging sources of growth. Active managers, by contrast, have the flexibility to adapt by allocating capital to new opportunities, managing emerging risks, and repositioning portfolios as leadership evolves.

A complementary approach to portfolio construction

forming a foundation for portfolio construction, active strategies complement this by seeking to enhance returns, manage risk and allocate capital more dynamically.

The key decision for investors is therefore not whether passive investing has merit, it clearly does, but rather how large a role passive exposure should play in the current market environment, and when to increase exposure to active strategies.

- First, concentration within major equity indices has increased significantly, making market outcomes more dependent on a relatively small number of companies.

- Second, differences in valuations and growth prospects between sectors and individual companies have widened, creating greater dispersion in potential returns.

- Third, the global economy is undergoing a period of structural adjustment driven by technological disruption, geopolitical realignment and evolving supply chains.

Passive investing, meanwhile, remains an effective way to gain broad market exposure, but tends to mirror the market as it exists today, along with its concentrations, imbalances, and momentum.

At a time when the world is rapidly evolving, relying solely on index exposure risks anchoring portfolios too heavily to yesterday’s winners. Increasing exposure to disciplined, research-driven active strategies introduces the flexibility to manage concentration risk, identify emerging opportunities, and adapt as market leadership evolves.

In our view, positioning for the next phase of the market cycle calls for a deliberate tilt toward active management, and with it, the ability to manage risk more effectively while capturing new opportunities as they arise.

All information and opinions provided are of a general nature and are not intended to address the circumstances of any particular individual or entity. We are not acting and do not purport to act in any way as an adviser or in a fiduciary capacity. No one should act upon such information or opinion without appropriate professional advice after a thorough examination of a particular situation. We endeavour to provide accurate and timely information, but we make no representation or warranty, express or implied, with respect to the correctness, accuracy or completeness of the information and opinions. Forecasts or commentary about expected future asset class or market performance in general are based on disclosed reasonable assumptions and not a reliable indicator of future results. We do not undertake to update, modify or amend the information on a frequent basis or to advise any person if such information subsequently becomes inaccurate. Any representation or opinion is provided for information purposes only. Ninety One Investment Platform (Pty) Ltd, Ninety One SA (Pty) Ltd and Sanlam Investment Management (Pty) Ltd (which forms part of the Ninety One group of companies) are authorised financial services providers. Additional important information and Disclosure Statements in terms of the Financial Advisory and Intermediary Services Act, 2002 can be found on the Ninety One website. Except as otherwise authorised, this information may not be shown, copied, transmitted, or otherwise given to any third party without Ninety One’s prior written consent. © 2026 Ninety One. All rights reserved. Issued by Ninety One.