Market and Economic Summary

Global markets continued their downward trend this month, posting another negative performance. Global equity markets recorded their third consecutive negative return this month, as sentiment toward risk assets waned. The “higher for longer” theme continued to dominate in October, as strong economic data, and upside risks to inflation continued to signal to market participants that interest rates may stay higher for longer. Inflation concerns were further exacerbated by the continued conflict in the Middle East. Given the risk off environment, safe haven assets such as gold and the US dollar strengthened this month, as investors sought refuge in a particularly volatile environment. The risk off environment did not spare US bonds, as yields continued upwards, recording their sixth consecutive month of increases, leading prices lower.

While most developed market policymakers concluded their meetings in September, the European Central Bank (ECB) held its meeting in October and followed most central banks by keeping interest rates at multi-year highs. This decision not to hike interest rates marked a shift from its 15-month streak of rate hikes and indicated a more cautious “wait-and-see” stance among policymakers. The central bank mentioned that it is determined to ensure inflation returns to its 2% target over the medium term, saying it will maintain interest rates at these elevated levels for a sufficiently extended period until it achieves that objective. As we head into November, where there are a few developed market central bank meetings, all eyes will be on the key decision makers as they grapple with inflation and robust economic data.

Developed market inflation numbers largely remained at similar levels to the prior month, fueling concerns of inflation remaining “higher for longer”. The annual inflation rate in the US remained at 3.7% (year-on-year to the end of September) from 3.7% in August and above market forecasts of 3.6%. The core inflation rate, however, slowed for the sixth month to 4.1% (year-on-year to the end of September), as key drivers such as shelter, and services continued to decline. China’s consumer prices remained unchanged in September, below market forecasts of 0.2%. The latest data indicated persistent deflationary pressures in the world’s second-largest economy, raising concerns about the sustainability of the economic recovery due to decreased demand. The inflation rate in the euro area declined to 2.9% (year-on-year to the end of September), reaching its lowest level since July 2021 and falling below the market consensus of 3.1%. Consumer price inflation in the United Kingdom remained at 6.7% (year-on-year to the end of September), from 6.7% in the previous month, below the market consensus of 6.8%.

Turning to other key economic data releases this month. The US continued to produce robust economic data in October, leading to concerns of further leeway for the US Federal Reserve to leave borrowing costs at restrictive levels for a prolonged period. The US economy expanded 4.9% (year-on-year in the third quarter of 2023), above market forecasts of 4.3%. The labour market in the US continues to remain tight, with the unemployment rate at 3.8% in September of 2023, slightly above market expectations of 3.7%. Retail sales in the US advanced 0.7% (month on-month in September), beating forecasts of a 0.3% advance. The data continues to point to robust consumer spending despite high prices and borrowing costs.

South African asset classes followed global peers lower this month, as local equities came under pressure. South African equities were not spared in the global sell-off and reported a negative return for the month, broadly in line with the emerging market complex. South African bonds defied the global trend and posted a positive return this month and were one of the few local asset classes to end the month in positive territory. The rand strengthened this month, despite a broadly stronger US dollar.

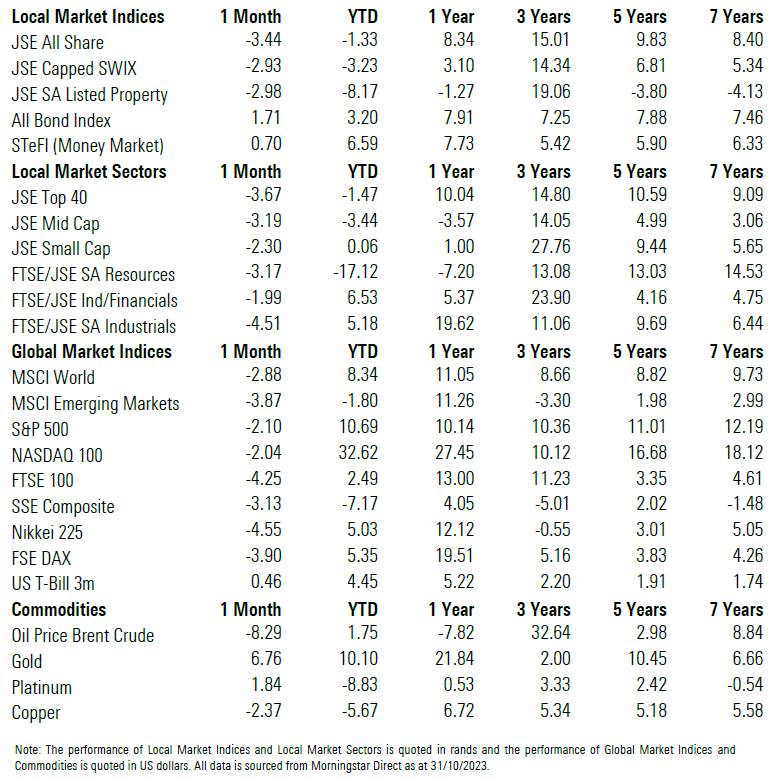

The weakness in South African equities was broad based, as all sectors produced negative returns. Industrials were the largest laggard as index heavy weight MTN (-19.4%) fell on weak results and concerns around exposure to Nigeria. Further to that, certain rand hedges including Richemont (-3.9%), Prosus (-5.4%) and British American Tobacco (-5.5%) fell on the back of a firmer rand and generally weak global equity markets. Financials produced a negative return this month, however, the return was largely ahead of the broader market weakness. After a robust month in September, Resources produced a significantly weaker October performance, on the back of weakness in platinum and diversified miners. On the other hand, gold counters such as Harmony (+22.7%), Gold Fields (+21.0%) and Anglogold (+13.1%) produced robust returns this month as the gold price moved higher (+6.8%).

Local bonds ended the month higher, as the yield curve bull steepened, with short term yields falling faster than longer term yields. The strength in the SA bond market suggests that investors are becoming more comfortable that the market is pricing in much of the bad news associated with the fiscal outlook.

Local listed property produced a negative performance this month, however, the performance was ahead of the SA equity market. The prevailing risk-off sentiment, coupled with a large decline in the index heavy weights Nepi Rockcastle (-2.8%) and Growthpoint (-1.4%) led the sector lower.

South Africa’s annual inflation rate moved sharply higher to 5.4% (year-on-year to the end of September), above market estimates, with the increase in the fuel price being the largest contributor.

The annual core inflation, which excludes prices of food, non-alcoholic beverages, fuel and energy, eased to a 13-month low of 4.5% (year-on-year in September 2023), below market forecasts of 4.7%. The sharp increase in headline inflation was largely on the back of the increased fuel price, however, given the recent oil price movements (and subsequent petrol price cuts expected for November), all eyes will be on the next inflation print.

The South African Chamber of Commerce and Industry (SACCI) business confidence index fell marginally to 108.2 in September 2023, compared to the August figure of 108.6. Factors such as energy supply constraints and inflation negatively affected sentiment, whereas foreign business-related elements had a positive influence. According to SACCI “the current business climate is not conducive to stimulating overall economic activity”.

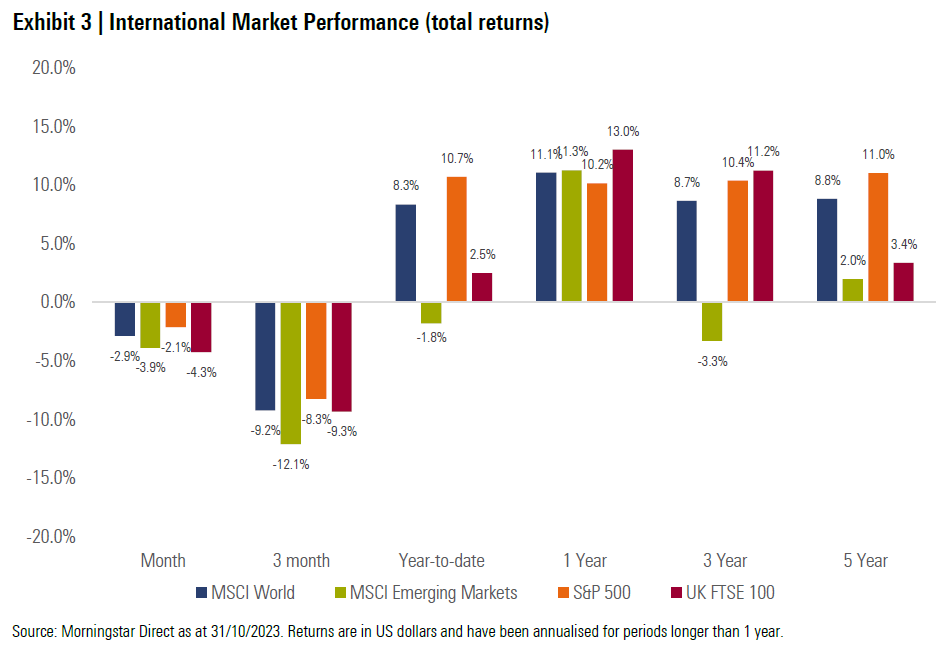

Most of the major developed equity markets ended the month lower this month. The MSCI World Index delivered a return of -2.9%, which was ahead of emerging market peers.

Most emerging equity markets moved lower during the month, on the back of waning appetite for risk assets. The MSCI Emerging Markets Index ended the month -3.9% lower in October.

All major global equity markets produced negative returns in October. The UK’s FTSE 100 (-4.3%), Germany’s FSE DAX (-3.9%), Japan’s Nikkei 225 (-4.6%) and China’s Shanghai SE Composite (-3.1%) ended the month in negative territory.

US equities moved lower in October, following global peers. The tech-heavy NASDAQ 100 (-2.0%) posted a negative performance as mega-cap technology stocks came under pressure, however, on a year-to-date basis the performance is still very strong. The S&P 500 (-2.1%) also ended the month lower, as most sectors ended in negative territory.

From a portfolio perspective, investors struggled to generate meaningful performance in a particularly weak environment during the month of October. Negative global sentiment towards risk assets pushed South African equities lower this month. On the other hand, the strong local bond market provided a buffer to the local and global market weakness. Global equity markets generated weak hard currency returns this month, on the back of negative sentiment towards risk assets. Rand strength acted as a further headwind to the performance of global allocations, as the local unit was firmer against most of the major crosses during the month.

After the volatile and particularly weak moves of October, we are reminded that economic events such as possible recessions, geopolitical tensions and the uncertainties that come with it bring out behavioural biases and focuses investors on the short term. Moreover, it reinforces the need for robustness and diversification in portfolios. Specifically, we continue to seek exposure to assets that offer strong forward-looking prospects, while balancing risks with defensive exposures.

We remain comfortable with the current positioning of client portfolios, both from an asset allocation and a manager selection perspective. We will continue to follow our valuation-driven approach by allocating assets to the most attractive areas of the market from a reward-for-risk perspective and ensure we build robust portfolios. We are confident that we will continue to deliver on the specific investment objectives of each client portfolio independent of the prevailing market environment.

Morningstar’s Investment Management group, through its investment advisory units, creates investment solutions that combine award-winning research and global resources with proprietary Morningstar data. Morningstar’s Investment Management group provides comprehensive retirement, investment advisory, and portfolio management services for financial institutions, plan sponsors, and advisers around the world.Morningstar’s Investment Management group comprises Morningstar Inc.’s registered entities worldwide including: Morningstar Investment Management LLC; Morningstar Investment Management Europe Limited; Morningstar Investment Management South Africa (Pty) Ltd; Morningstar Investment Consulting France; Ibbotson Associates Japan, Inc; Morningstar Investment Adviser India Private Limited; Morningstar Investment Management Asia Ltd; Morningstar Investment Services LLC; Morningstar Associates, Inc.; and Morningstar Investment Management Australia Ltd.About Morningstar, Inc.

Morningstar, Inc. is a leading provider of independent investment research in North America, Europe, Australia, and Asia. The company offers an extensive line of products and services for individual investors, financial advisors, asset managers, retirement plan providers and sponsors, and institutional investors in the private capital markets. Morningstar provides data and research insights on a wide range of investment offerings, including managed investment products, publicly listed companies, private capital markets, and real-time global market data. The company has operations in 27 countries.

Important Information

The opinions, information, data, and analyses presented herein do not constitute investment advice; are provided as of the date written; and are subject to change without notice. Every effort has been made to ensure the accuracy of the information provided, but Morningstar makes no warranty, express or implied regarding such information. The information presented herein will be deemed to be superseded by any subsequent versions of this document. Except as otherwise required by law, Morningstar, Inc or its subsidiaries shall not be responsible for any trading decisions, damages or losses resulting from, or related to, the information, data, analyses or opinions or their use. Past performance is not a guide to future returns. The value of investments may go down as well as up and an investor may not get back the amount invested. Reference to any specific security is not a recommendation to buy or sell that security. There is no guarantee that a diversified portfolio will enhance overall returns or will outperform a non- diversified portfolio. Neither diversification nor asset allocation ensure a profit or guarantee against loss. It is important to note that investments in securities involve risk, including as a result of market and general economic conditions, and will not always be profitable. Indexes are unmanaged and not available for direct investment.

This commentary may contain certain forward-looking statements. We use words such as “expects”, “anticipates”, “believes”, “estimates”, “forecasts”, and similar expressions to identify forward-looking statements. Such forward- looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results to differ materially and/or substantially from any future results, performance or achievements expressed or implied by those projected in the forward-looking statements for any reason.

The Report and its contents are not directed to, or intended for distribution to or use by, any person or entity who is not a citizen or resident of or located in any locality, state, country or other jurisdiction listed below. This includes where such distribution, publication, availability or use would be contrary to law or regulation or which would subject Morningstar or its subsidiaries or affiliates to any registration or licensing requirements in such jurisdiction.

The Report is distributed by Morningstar Investment Management South Africa (Pty) Limited, which is an authorized financial services provider (FSP 45679), regulated by the Financial Sector Conduct Authority.