The performance of global markets provided some reprieve to investors in October, as developed equity markets recovered from their year-to-date lows recorded in September. Whilst global markets continue to face multiple headwinds, the consensus was that equity markets were reaching over-sold territory and investors’ sentiment improved towards risk assets, particularly European and US equities. Global bonds, on the other hand, had another negative month, as investors continued to price in future interest rate increases, leading global bonds to their thirteenth straight negative month of performance. The standout underperformer during the month was Chinese equities, which fell significantly. The weakness in China was largely on the back of the Chinese National Party Congress, where President Xi Jinping was granted a third term and fixed his leadership ranks with a group of loyalists, stoking fears of his unfretted ability to enact policies which may not be market friendly.

Global inflation prints continue to remain elevated, with core inflation continuing to tick higher. The annual inflation rate in the UK moved back to a 40-year high of 10.1% (year-on-year to the end of September), from 9.9% in August. Euro area inflation increased marginally to 10.7% (year-on-year to the end of

October), to yet another record high, as energy costs remain elevated. US headline inflation eased for a third straight month to 8.2% in September of 2022, from 8.3% in August. On the other hand, US core inflation continued to remain elevated and printed at 6.6% (year-on-year to the end of September), ahead of market expectations. China’s annual inflation rose to 2.8% (year-on-year to the end of September) from 2.5% in August.

Central banks continue to target inflation by aggressively hiking interest rates, with more interest rate hikes pencilled in for November. During its October meeting, the European Central Bank raised interest rates by 0.75%, matching expectations from most analysts and bringing borrowing costs to the highest

since early 2009. The job market remains robust, as developed markets continue to post low unemployment rates. During October, the US posted its unemployment rate at 3.5%, below expectations of 3.7%, while the UK unemployment rate was 3.5%, its lowest rate since 1974.

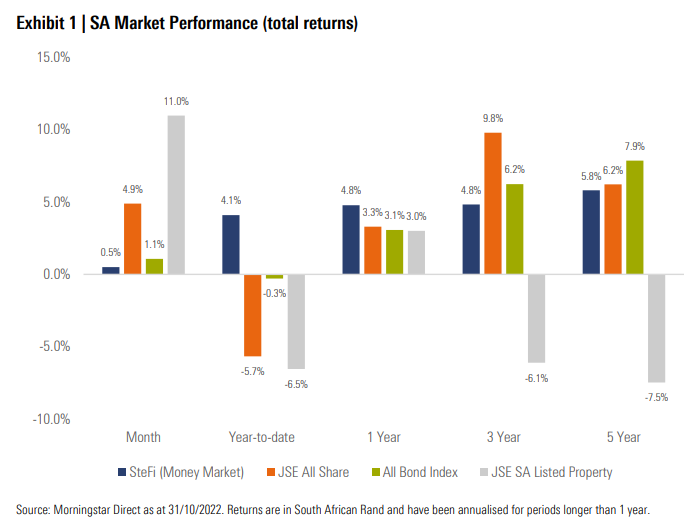

South African asset classes followed developed market peers and posted robust returns, outperforming the emerging markets complex.

South African equities ended October higher, with all sectors posting a positive performance. Financials rebounded significantly and is the top performer over the past twelve months. Industrials posted a positive performance, albeit lagging the broader market, given the significant negative moves posted by Naspers and Prosus. Resources posted a positive performance on the back of a firmer industrial metals complex price, and a weaker rand.

Local bonds ended the month higher and fared better than their developed market peers. The nominal yield curve remained roughly where it started the month, with prices on the short end of the curve shifting higher (as yields fell), in line with expectations of a moderation in interest rate hikes.

Local listed property rebounded strongly in October, posting double digit returns, with the market heavy weights leading the rebound.

South Africa’s annual inflation rate eased for a second month to 7.5% (year-on-year to the end of September) from an over 13-year high of 7.8% recorded in July, driven largely by a decrease in the fuel price. Inflation, however, remains above the upper limit of the South African Reserve Bank’s target range

of 3%-6%. However, in line with global peers, the annual core inflation rate increased to a five-year high of 4.7% in September.

During the month, the National Treasury delivered the Medium-Term Budget Policy statement, which outlined the targets over the next three years. Due to higher commodity prices, tax revenue collection has been revised higher by R83.5bn and total main budget revenue has been revised higher by R106.4bn for the 2022/23 fiscal year. On the expenditure front, National Treasury outlined R30bn funding to Denel, Transnet and Sanral and R6.4bn to Kwazulu Natal in order to assist the province with flood damage from earlier in the year.

National Treasury announced that they will be taking on a significant portion of Eskom’s debt (currently R400bn). Other significant announcements were that the Covid-19 social relief grant would be extended to 31 March 2024, the government wage bill will be increased by 3% annualized over the next four fiscal years and the Treasury will do everything possible to avoid being grey-listed.

South Africa’s SACCI Business Confidence Index rose to 110.9 in September, from 105.6 in the previous month. It was the highest reading since February, as there was an increase in tourism and trade volumes.

Most of the major developed equity markets ended the month in positive territory, after the broad declines seen in September. The MSCI World Index delivered a return of +7.2% in October, ahead of its emerging market peers.

Emerging market equities underperformed developed market equities in October, as Chinese equities led the decline over the month. The MSCI Emerging Markets Index ended the month -3.1% lower in October.

Most major global equity markets rebounded in October, barring China. The UK’s FTSE 100 (+6.2%), Germany’s FSE DAX (+10.4%) and Japan’s Nikkei 225 (+3.6%) all delivered positive performance for the month. China’s Shanghai SE Composite (-7.1%) continued to come under pressure in October.

US equities ended the month higher in October. The US equity rebound was relatively broad based, with the S&P 500 (+8.1%) leading the rebound. The tech-heavy NASDAQ 100 (+4.0%) ended the month higher but lagged the broad market as large US tech companies’ results came in lower than expected.

Impact on client portfolios

Following the negative performance in August and September, markets provided some reprieve to investors in October as markets started the fourth quarter strongly. From a portfolio perspective, most portfolios managed to generate positive performance over the month. Rand weakness over the month

provided a tailwind to the performance of global asset classes. Global emerging markets exposure (in particular China exposure) and global bond exposure hurt performance this month.

We remain comfortable with the current positioning of client portfolios, both from an asset allocation and a manager selection perspective. We will continue to follow our valuation driven approach by allocating assets to the most attractive areas of the market from a reward for risk perspective and ensure we build robust portfolios. We are confident that we will continue to deliver on the specific investment objectives of each client portfolio independent of the prevailing market environment.