Market and Economic Summary

In May, global markets experienced a more subdued performance, with the majority of global equity markets ending lower. A major exception was the US equity market, driven higher by the tech sector, which saw significant gains during the month, primarily driven by mega-cap tech stocks. Despite generally positive economic data from developed markets, market participants were concerned about the uncertainty surrounding the lifting of the US debt ceiling during the month. In the end, the US debt negotiations concluded without major disruptions, as house representatives voted in favour of lifting the debt ceiling, thus easing concerns of a US default. However, the uncertainties surrounding this issue resulted in significant volatility across most risk assets during the month. Central bank actions were largely in-line with expectations, as central banks continued to hike rates albeit at a more subdued pace, suggesting that many developed nations are potentially nearing the end of their hiking cycles.

Inflation remained elevated and above most central banks’ inflation targets. However, inflation has been trending lower over the past few months. The Euro Area’s consumer price inflation rose 7.0% (year-on-year to April 2023), slightly higher than the previous month’s reading of 6.9%. Euro Area core inflation, on the other hand, eased slightly to 5.6% but remained near the all-time high of 5.7%. The annual inflation rate in the US fell to 4.9% (year-on-year to the end of April), the lowest since April 2021, and below the consensus forecast of 5%. China’s annual inflation rate fell to 0.1% (year-on-year to the end of April 2023) from 0.7% in the previous month, below consensus estimates of 0.4%. This was the lowest inflation print in China since 2021 amid an uneven economic recovery after the removal of a zero-COVID policy, with prices of both food and non-food items easing further. The consumer price inflation in the UK fell to 8.7% year-on-year in April 2023, the lowest since March 2022, due to a sharp slowdown in electricity and gas prices. However, the inflation rate exceeded consensus expectations of 8.2% and remains well above the Bank of England’s target rate of 2.0%.

Policymakers continued to signal a slowing pace of policy tightening as borrowing costs have increased to levels last seen prior to the Global Financial Crisis in 2008. In the US the Fed raised the fed funds rate by 0.25% to a range of 5%-5.25% during its May meeting, marking the 10th increase and bringing borrowing costs to their highest level since September 2007. The European Central Bank (ECB) raised its key interest rates by 0.25% during its May meeting, signalling a slowing pace of policy tightening. Borrowing costs in Europe have now reached their highest level since July 2008, following seven consecutive rate increases as the ECB strives to combat high inflation despite ongoing recession risks. The Bank of England raised rates by 0.5% to 4.5% in May 2023, marking the twelfth consecutive rate increase, pushing borrowing costs to levels not seen since 2008.

Turning to the jobs market, developed markets’ unemployment rates continue to remain at or close to historic lows, providing more room for central banks to move rates higher to curb inflation. The unemployment rate in the Euro Area decreased slightly to 6.5% (at the end of March 2023) marking the lowest rate on record and coming in just below expectations of 6.6%. The tight labour market gives the European central bank more leeway for policy tightening. The unemployment rate in the United States edged down to 3.4% (at the end of April 2023), below expectations of 3.6%. The unemployment rate in the United Kingdom experienced a slight increase to 3.9% (at the end of March 2023) slightly above the consensus expectation of 3.8%.

South African asset classes produced mostly negative returns this month. Local equities and bonds produced poor returns in May, as intense load shedding and increased diplomatic tensions dampened sentiment towards South African assets.

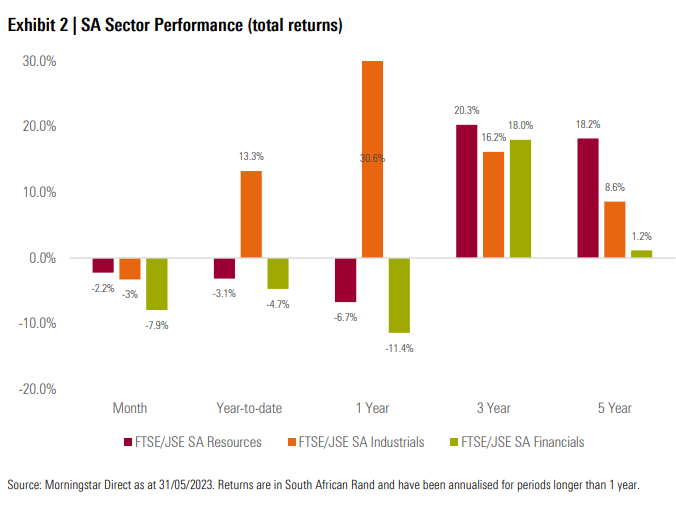

South African equities ended the month lower, as all sectors produced negative returns. Financials were the biggest laggard this month, dragged down by performances of index heavyweights Capitec (-13.7%) and Firstrand (-6.4%). Resources produced a resilient albeit negative return this month, as gold shares and rand hedges produced a resilient performance. Industrials ended lower dragged down by retailers Spar (- 24.7%), Mr Price (-17.5%) and Pepkor (-16.8%), who all moved significantly lower this month.

Local bonds ended the month lower, producing their fourth worst return in 22 years, as yields shifted higher across the curve leading prices lower. The negative move was largely on the back of the hawkish tone from the South African Reserve Bank (SARB) as they continued to hike rates to tame elevated inflation. Poor sentiment towards South Africa also saw foreigners being net sellers of South African bonds every day of the month of May.

Local property followed other South African asset classes lower. Europe focused counters outperformed this month, producing strong returns as the rand weakness provided a tailwind to their performance.

The SARB increased rates by 0.5% to 8.25% during its May meeting, the 10th consecutive increase in interest rates, pushing borrowing costs to their highest level since May 2009. Policymakers cited concerns regarding the depreciation of the rand and the second-round impacts on inflation as reasons behind the rate adjustment. The SARB also revised its inflation forecasts upwards with inflation now projected to average 6.2% in 2023, higher than the original estimate of 6.0%.

South Africa’s annual inflation rate followed the global trend lower and fell to an 11-month low of 6.8% (year-on-year to the end of April 2023) down from 7.1% in March and below market forecasts of 7%. Inflation continues to be above the upper limit of the SARB’s target range of 3%-6%. On the other hand, core inflation rose to a six-year high of 5.3% (year-on-year to the end of April), up from 5.2% in March.

South Africa’s unemployment rate moved higher to 32.9% in the first quarter of 2023, the first rise in over a year. The expanded definition of unemployment, which includes those discouraged from seeking work, was 42.4% in Q1, down from 42.6% in the fourth quarter. The youth unemployment rate, measuring jobseekers between 15 and 24 years old, rose to 62.1% in Q1, from 61% in the previous three-month period.

Most of the major developed equity markets ended the month lower this month. The MSCI World Index delivered a return of -0.9%, which was ahead of its emerging market peers.

Most emerging equity markets moved lower during the month, dragged down by China who fell on concerns of weak economic data. The MSCI Emerging Markets Index ended the month -1.7% lower in May.

Most major global equity markets produced negative returns in May. The UK’s FTSE 100 (-6.3%), Germany’s FSE DAX (-5.0%) and China’s Shanghai SE Composite (-6.0%) ended the month in negative territory. Japan’s Nikkei 225 (+4.3%) bucked the trend and rallied this month posting its best performance in 30 months.

US equities ended the month mostly higher driven largely by US tech. The tech-heavy NASDAQ 100 (+7.7%) ended the month higher as mega-cap tech shares posted strong gains. The S&P 500 (+0.4%) ended the month marginally higher driven by the mega-cap tech stocks. The positive performance and narrow market leadership masked the underlying negative returns of the majority of the stocks in the S&P 500 this month.

Impact on Client Portfolios

During the month of May, markets trended lower as market participants continued to focus on central banks’ actions to tame inflation whilst keeping an eye on the health of the global economy. Local equities ended the month lower in a particularly volatile month, while local bonds also moved lower. From a portfolio perspective, most portfolios struggled to generate a positive performance over the month, with portfolios allocated heavily to local bonds and equities moving meaningfully lower. Rand weakness over the month provided a tailwind to the performance of global asset classes.

We remain comfortable with the current positioning of client portfolios, both from an asset allocation and a manager selection perspective. We will continue to follow our valuation-driven approach by allocating assets to the most attractive areas of the market from a reward-for-risk perspective and ensure we build robust portfolios. We are confident that we will continue to deliver on the specific investment objectives of each client portfolio independent of the prevailing market environment.

About the Morningstar Investment Management Group

Morningstar’s Investment Management group, through its investment advisory units, creates investment solutions that combine award-winning research and global resources with proprietary Morningstar data. Morningstar’s Investment Management group provides comprehensive retirement, investment advisory, and portfolio management services for financial institutions, plan sponsors, and advisers around the world.Morningstar’s Investment Management group comprises Morningstar Inc.’s registered entities worldwide including: Morningstar Investment Management LLC; Morningstar Investment Management Europe Limited; Morningstar Investment Management South Africa (Pty) Ltd; Morningstar Investment Consulting France; Ibbotson Associates Japan, Inc; Morningstar Investment Adviser India Private Limited; Morningstar Investment Management Asia Ltd; Morningstar Investment Services LLC; Morningstar Associates, Inc.; and Morningstar Investment Management Australia Ltd.About Morningstar, Inc.

Morningstar, Inc. is a leading provider of independent investment research in North America, Europe, Australia, and Asia. The company offers an extensive line of products and services for individual investors, financial advisors, asset managers, retirement plan providers and sponsors, and institutional investors in the private capital markets. Morningstar provides data and research insights on a wide range of investment offerings, including managed investment products, publicly listed companies, private capital markets, and real-time global market data. The company has operations in 27 countries.

Important Information

The opinions, information, data, and analyses presented herein do not constitute investment advice; are provided as of the date written; and are subject to change without notice. Every effort has been made to ensure the accuracy of the information provided, but Morningstar makes no warranty, express or implied regarding such information. The information presented herein will be deemed to be superseded by any subsequent versions of this document. Except as otherwise required by law, Morningstar, Inc or its subsidiaries shall not be responsible for any trading decisions, damages or losses resulting from, or related to, the information, data, analyses or opinions or their use. Past performance is not a guide to future returns. The value of investments may go down as well as up and an investor may not get back the amount invested. Reference to any specific security is not a recommendation to buy or sell that security. There is no guarantee that a diversified portfolio will enhance overall returns or will outperform a non- diversified portfolio. Neither diversification nor asset allocation ensure a profit or guarantee against loss. It is important to note that investments in securities involve risk, including as a result of market and general economic conditions, and will not always be profitable. Indexes are unmanaged and not available for direct investment.

This commentary may contain certain forward-looking statements. We use words such as “expects”, “anticipates”, “believes”, “estimates”, “forecasts”, and similar expressions to identify forward-looking statements. Such forward- looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results to differ materially and/or substantially from any future results, performance or achievements expressed or implied by those projected in the forward-looking statements for any reason.

The Report and its contents are not directed to, or intended for distribution to or use by, any person or entity who is not a citizen or resident of or located in any locality, state, country or other jurisdiction listed below. This includes where such distribution, publication, availability or use would be contrary to law or regulation or which would subject Morningstar or its subsidiaries or affiliates to any registration or licensing requirements in such jurisdiction.

The Report is distributed by Morningstar Investment Management South Africa (Pty) Limited, which is an authorized financial services provider (FSP 45679), regulated by the Financial Sector Conduct Authority.