Market and Economic Summary

Most global markets moved higher in March, however, the positive moves masked the volatile nature of global financial markets over the month. The recent stress in the banking sector including SVB, Signature Bank and Credit Suisse led market participants to reevaluate future central bank actions in relation to fighting inflation, whilst still maintaining financial stability. At the beginning of the month, the stress in the banking sector led safe havens higher, as market participants became concerned about a possible fallout in the broader financial sector. However, towards the middle of the month, most central banks moved to dispel fears of a financial crisis by indicating their support for financial stability. This provided a level of comfort to investors, leading global markets higher, as investors repriced the likely future path of interest rates.

During the month, central banks continued to raise interest rates to rein in inflation, whilst monitoring the situation with certain banks in the financial sector. The European Central Bank (ECB) raised interest rates by 0.5%, in line with forecasts, pushing borrowing costs to the highest level since 2008. The ECB also reassured investors that the euro area banking sector is resilient, with strong capital and liquidity positions, and they stood ready to respond as necessary to maintain financial stability in the region. The US Federal Reserve (Fed) raised the fed funds rate by 0.25%, matching expectations and pushing borrowing costs to levels last seen in 2007, as inflation remains elevated. The Fed followed in the ECB’s footsteps, by reassuring investors that the US banking system is sound and resilient. The Bank of England raised its key bank rate by 0.25% to 4.25% during the March 2023 meeting, in line with expectations, and pushing borrowing costs to fresh highs since 2008, in response to elevated inflation.

Developed market inflation prints came in largely lower than expected, apart for the UK, which continues to sit in double digit territory. The annual inflation rate in the UK unexpectedly edged higher to 10.4% (year-on-year to the end of February), ahead of forecasts of 9.9%. Inflation in the euro area fell to 6.9% (year-on-year to the end of March), its lowest level since February 2022 and below market consensus of 7.1%. The cost of energy declined for the first time in two years (-0.9%). By contrast, inflation accelerated for food, alcohol and tobacco, which was one of the larger contributors to headline inflation. China’s annual inflation rate fell to 1.0% (year-on-year to the end of February). This was the lowest inflation print since February 2022, with prices for most categories easing sharply. The annual inflation rate in the US slowed to 6% (year-on-year to the end of February), the lowest since September of 2021, in line with market forecasts.

Turning to unemployment, developed job markets continue to remain robust, but the trend of unemployment seems to be upwards in certain regions. The unemployment rate in the US moved higher to 3.6% at the end of February 2023, above market expectations of 3.4%. The labour force participation rate moved higher to 62.5%, the highest since March 2020. The euro area unemployment rate was 6.6% at the end of February 2023, in line with estimates, and continues to be at a record low.

The unemployment rate in the UK was unchanged at 3.7% (at the end of January 2023), below expectations.

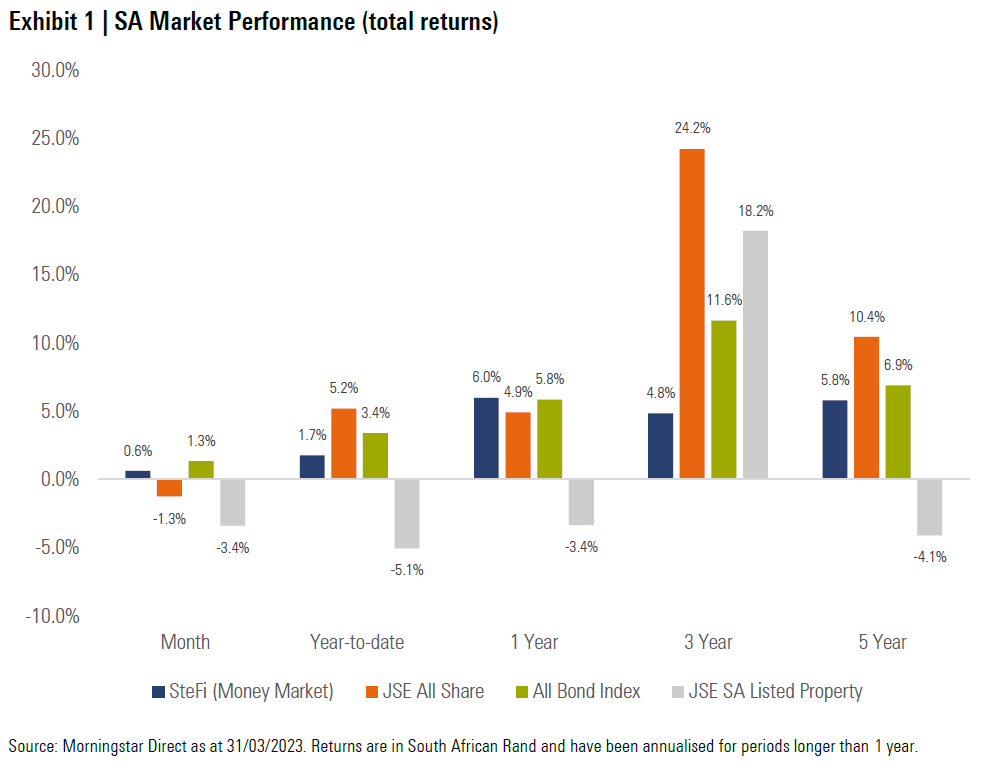

Some South African asset classes bucked the global trend and produced negative returns in March, as electricity shortages continued to dampen sentiment. Local equities ended the month lower, while local bonds on the other hand, produced positive returns.

South African equities ended the month mostly lower, as Financials came under significant pressure, following instability in the global banking sector, which caused an element of contagion in the local banking names. Resources bounced back in March after a difficult February, as resource prices (in particular gold prices) moved higher during the month. Gold Fields (+45.3%), Anglogold Ashanti (+40.4%) and Harmony Gold (+31.1%) were all beneficiaries of the elevated gold price, moving significantly higher in March. Industrials on the other hand, moved lower, but produced a resilient return on the back of index heavy weights Richemont and Prosus posting positive returns.

Local bonds ended the month higher, as the yield curve steepened in March. Yields came down (leading to higher prices) on the front end of the curve, while yields moved higher on the back end of the curve. The curve steepness did subside slightly towards the end of March, as the central bank raised interest rates by more than expected.

Local property ended the month lower and is the worst performing local asset class on a year-to-date basis. The weakness was broad based but was led by weak performance from index heavy weights Growthpoint (-2.8%) and Redefine (-4.7%).

In March, the South African Reserve Bank (SARB) surprised the market by raising its benchmark repo rate by 0.5% to 7.75%. This move marked the ninth consecutive interest rate hike since policy normalization began in November 2021, and brings borrowing costs to their highest level since May 2009. Policymakers now expect headline inflation of 6% for the 2023 calendar year, at the upper end of the inflation target band of between 3-6%.

South Africa’s annual inflation rate moved higher to 7% (year-on-year to the end of February 2023), ahead of expectations and the first rise in inflation since the back end of 2022. The main upward pricing pressure came from prices of food and non-alcoholic beverages, most notably bread and cereals, oils and fats, vegetables, and transportation. The annual core inflation rate continues to be elevated and increased to 5.2% (year-on-year to the end of February), the highest since February 2017.

South Africa’s economy advanced by 0.9% (year-on-year in the fourth quarter of 2022), the lowest in seven quarters, and below market estimates of 2.2%. This came on the back of multiple factors, one being the continued electricity disruption which continues to be detrimental to economic growth.

The first quarter of 2023 saw a decline in the FNB/BER Consumer Confidence Index for South Africa, dropping to -23 points from the previous quarter’s two-year high of -8 points. This marks the third-lowest reading on record since 1993, indicating significant levels of concern among consumers about both the country’s economic outlook and their own financial situations.

Most of the major developed equity markets ended the month higher, producing strong gains for the first quarter of 2023. The MSCI World Index delivered a return of +3.2% in March, which was slightly ahead of its emerging market peers.

Most emerging equity markets moved higher during the month. The MSCI Emerging Markets Index ended the month +3.1% higher in March.

Most major global equity markets produced positive returns in March. Japan’s Nikkei 225 (+5.5%), Germany’s FSE DAX (+4.2%) and China’s Shanghai SE Composite (+0.8%) ended the month in positive territory. The UK’s FTSE 100 (-0.4%) was one of the few global equity markets to end the month in negative territory.

US equities ended the month higher and ahead of most global peers. The tech-heavy NASDAQ 100 (+9.5%) ended the month significantly higher and has produced a robust double digit quarterly return. The S&P 500 (+3.7%) ended the month higher, however, the positive performance masked the significant volatility in US listed equities over the month.

Impact on Client Portfolios

During the month of March, markets experienced significant volatility and produced divergent returns across the local and global opportunity set. Global equities moved higher after a volatile month, while local equities struggled to produce meaningful returns. From a portfolio perspective, most portfolios struggled to generate positive performance over the month, with portfolios allocated heavily to local equities moving meaningfully lower. Rand strength over the month provided a headwind to the performance of global asset classes.

As we head into the new quarter, volatility and uncertainty continues to concern the market. Inflation, the continued slowdown in most global economies and the contagion from the recent banking market stress, continues to create massive uncertainty in the market. Despite the uncertainties ahead, it’s important to safeguard long-term wealth by constructing well-diversified portfolios with assets that are reasonably priced.

We remain comfortable with the current positioning of client portfolios, both from an asset allocation and a manager selection perspective. We will continue to follow our valuation driven approach by allocating assets to the most attractive areas of the market from a reward for risk perspective and ensure we build robust portfolios. We are confident that we will continue to deliver on the specific investment objectives of each client portfolio independent of the prevailing market environment.