Look across the valley. What do we have to look forward to beyond current performance.

By Victoria Reuvers, Managing Director, Morningstar Investment Management South Africa

Just as we thought Covid-19 was behind us, 2022 bombarded us with an array of new curve balls. From the war in Ukraine, inflation last seen in the 70s, rising interest rates and global markets experiencing drawdowns that rank as one of the worst on record, investors had very little (if any) place to hide.

It almost feels like there’s a new headline about a new disaster happening somewhere around the world every day and quite frankly, it’s rather depressing.

In the words of Peter Lynch, “You can’t see the future through a rearview mirror.” Imagine having to drive your car up a steep hill, with numerous bends and turns, not looking through your windshield and only being guided by the view in your rearview mirror – it’s a pretty terrifying thought. Given that we drive by looking out the windscreen and not by looking in the rearview mirror, I want to change how we are looking at this crisis.

Yes, things are bad and there is a range of factors to support this. Market returns year to date are terrible and I don’t think anyone is looking at their statement with a smile on their face. However, these performance figures are what is currently visible through our rearview mirror, and not our windshield. What is important is what lies ahead and how we as investors are positioned to recoup losses and generate wealth.

Is there anything to look forward to?

Predicting the future is not a skill possessed by investment professionals. We thus pay very little attention to market predictions. We honestly have no idea what will happen with regard to politics, economics and short-term currency and market movements. So, what do we know….

1) For the first time in over a decade, investors are being rewarded for owning bonds.

The reaction of central banks to raise interest rates on the back of inflation is painful but it is the medicine the market needed – a reset to an environment where asset classes are fairly priced. Medicine is rarely easy to swallow but it is a necessary remedy.

In terms of drawdowns, global bonds have behaved similarly to equities this year. With that said, bonds tend to recover losses and generate positive returns before equities when we are at the top of the interest rate cycle. Most people are trying to figure out when that cycle ends. We don’t believe anybody knows, however, what we do know is that long-dated bonds typically generate solid positive returns at the end of the cycle.

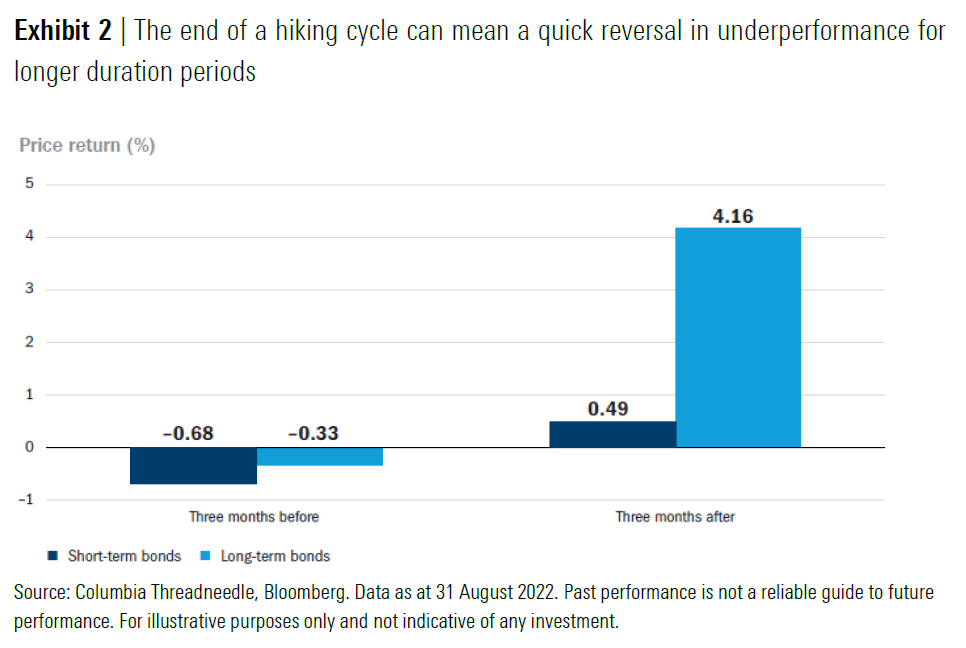

The below graph shows the return of bonds three months before and after a rate hiking cycle ends. As can be seen in this graph, returns on both short-duration and long-duration bonds are negative. However, in the three months after a rate hiking cycle ends, returns for long-duration bonds are especially sizeable.

In this graph,

• Short-term bonds are represented by two-year U.S. treasury notes.

• Long-term bonds are represented by 30-year U.S. treasury bonds.

• Performance is calculated using month-end returns for the three months before and after the Fed reaches the peak of its hiking cycle.

2) Central banks are doing their job – slowly but surely

Maybe some have been a bit slow and some are not moving as quickly as we would like to see but they are moving. Credit must be given to the South African Reserve Bank in particular for its discipline and prudence when it comes to inflation targeting. Their strict adherence to their mandate often places short-term strain on South Africans however over the long term it ensures correct asset pricing and controlled inflation.

As a South African you can get a real yield of almost 4% despite inflation being at these levels. Compare that to the US, where bonds are offering a negative real yield of -6% despite the rise in interest rates.

3) Companies may go out of business but industries generally don’t

This year has seen broad-based equity price declines. Should these declines continue at their current rate it will rank as one of the worst years on record for equity investors. While there were definitely sectors and segments of the market that were overpriced coming into 2022, we do believe there has been contagion across all sectors and markets, leaving some very attractive investment opportunities for investors that are patient and prepared to look

beyond the noise.

The baby has been thrown out with the bath water. There is no substitute for fundamental analysis and understanding the price that you are paying for an asset and its future cash flows. No matter the quality of the company, future returns are dependent on the price you pay.

A good way to look at it is to look at the starting prices versus the price-to-earnings (PE) ratio of the market over time and to look at the subsequent five-year returns. There is clear evidence to show that your future return is heavily influenced by your starting price.

Based on where valuations are today, the future is looking bright. Currently, valuations are a poor timing tool and when we say ‘future’, we are looking at three years plus. Over the next week, month and/or year, there could be continued volatility, but the key is to look across the valley.

4) A weak dollar is a curse if you are a South African travelling abroad but a blessing for many other industries

Tourism, mining and agriculture benefit from a weaker rand. We often view the Rand/Dollar exchange rate as a test for how we feel about South Africa – when the rand is strong, we feel great about the prospect of the country, but when the rand is weak, pessimism tends to sink in.

It’s prudent to keep in mind that with every extreme move, someone benefits. The benefits to South Africa include contributing to GDP growth and employment. For every eight tourists, one permanent job is created. As we sell our resources in USD, the weaker rand helps to boost the country’s current account through the increased profits made from exports. While we do believe the dollar is overvalued and the rand is extraordinarily cheap, these disconnects can exist for some time, but they are not always negative. With this being said, while it has benefitted domestic portfolios year to date, a weaker dollar (and stronger rand) could have the reverse effect

So, what does this all mean?

This year is going to be a year filled with new records for markets, sadly not the good ones. Perspective is important as well as our ability to remove emotion from our investments as we go into 2023.

Statement values may be lower at this point in time but wealth is only destroyed and capital lost if you exit and crystalize the paper losses. While it feels like doom and gloom are abundant, so too are opportunities. Markets are forward-looking and the reality of the high inflation and interest rates that we are all experiencing is already in the price of portfolios.

This is not the time to make changes. This is the time to ignore your statement(s) and trust your long-term investment plan.

You don’t have to outsmart the market if you can simply outperform it. Cut through the confusion and noise and focus on what actually matters – a simple, consistent diversified approach over the long term and remember:

• Returns don’t happen in straight lines and it seldom occurs when one expects them to.

• The long term is just a collection of short runs and having a long-term strategy does not excuse you from the short-term setbacks in markets and funds.

• It’s vital to separate emotion from an investment portfolio. Often the most beleaguered investments turn out to be a great opportunity for future returns,

as investors can access these investments at a good price.

• Volatility creates opportunity and short-term underperformance can translate into a solid, longer-term upside.

For those still investing, the outlook is improving as lower prices could potentially imply higher future returns.