- Keep it Simple.

99% of long-term investing is doing nothing…

By Roné Swanepoel, Business Development Manager, Morningstar Investment Management South Africa

“It’s not whether you’re right or wrong that’s important, but how much money you make when you’re right and how much you lose when you’re wrong.” — George Soros

Let’s start with a thought experiment. If you look back on your investment journey to date, and the various hot tips you received – either via the media reporting the latest market craze, or something as simple as a friend’s hot tip at a Saturday braai. How many times did you act and buy into these hot tips? How many times did it pay off? Are you possibly still invested in one of these stocks, sectors or funds? With the benefit of hindsight, are you happy you invested when you did?

Although these hot tips work out well for some, they are often handed out when the particular stock, fund or sector has already gained and reached its peak in popularity. It seldom occurs, as with all market timing, that investors receive this tip when the price is still low, enabling them to buy in at a reasonable price to realise a decent profit.

We make some of our worst decisions by paying too much attention to opinions about markets where many of the variables are either unimportant or unknowable when it comes to our investments.

As markets turn more volatile and create uncertainty – as we have seen in the last year – opinions become louder, the pressure in the market mounts and the headlines start jumping out at us begging us to try and time the market. Headlines like “Markets and the economy to face a meltdown in 2023”, “The best stocks to profit from the AI trade”, “Market guru says his ‘once in a decade’ trade is upon us,” or “Reasons why you should move all your money away from South-Africa”. We must remember there are two sides to any coin.

When very persistent narratives are so visible, it becomes very difficult for investors to focus on anything else, and to ignore these narratives. We become gripped with the things we don’t know and it becomes increasingly difficult to pick a good mix of funds for your investment portfolio – and avoid making big changes to it. But you should. As Morgan Housel once wrote, “99% of long-term investing is doing nothing…”

The power of doing nothing

Over the long term the stock market rises in value. Corporations like making profits. Money must go somewhere and people like the returns they get in the stock market. Simple.

The one factor that remains constant is that to derive these positive returns, you have to be invested. Unfortunately, that involves staying invested through periods when markets go up and down. Why? Because no one can accurately and consistently time the market.

Although we know the stock market trends up over time, the graph is never linear and constantly punctuated by turbulence, rallies and dips as can be seen in the chart below showing the S&P 500 index since the 1940s.

Time in the market, versus timing the market

Timing is the bane of investors everywhere. We fear buying or selling at the wrong time. Given the volatility in markets, bad timing can cost you dearly.

Let’s illustrate this using a local example.

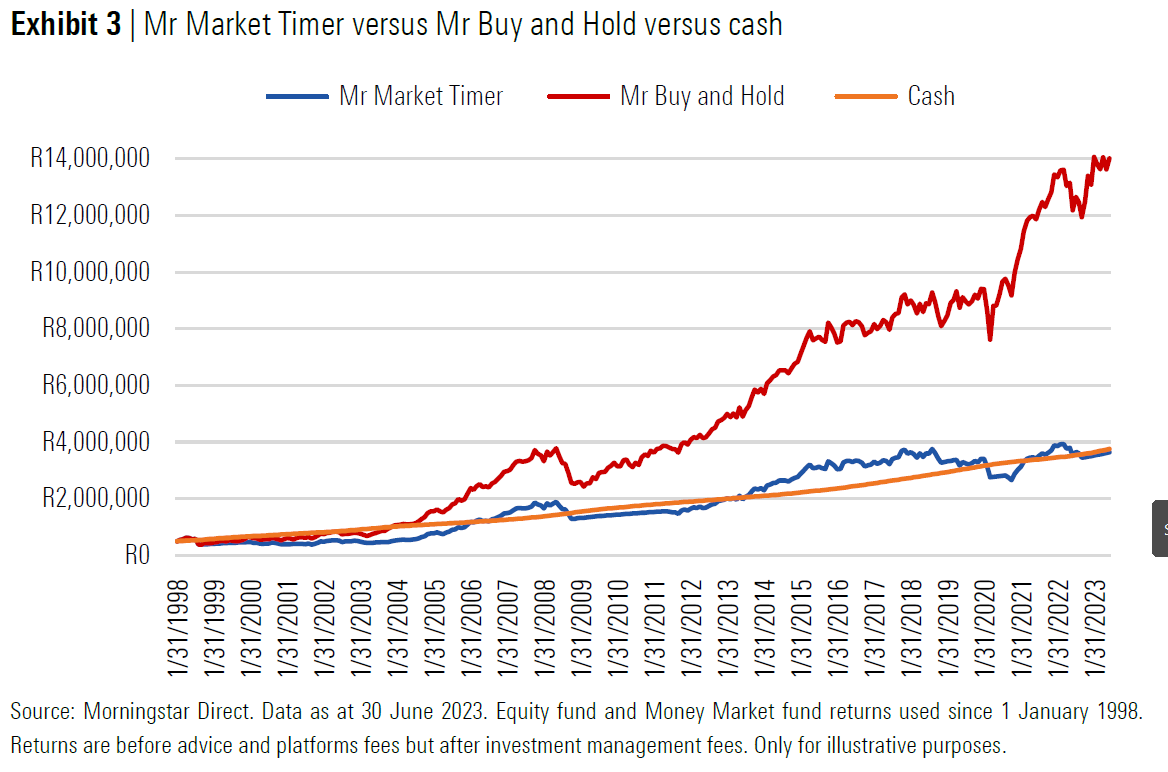

- We have two investors: “Mr Market Timer” and “Mr Buy and Hold” – both have R500 000 to invest.

- They are both high-risk investors and would like to invest in a local equity fund.

- They both start their investment journey on 1 January 1998.

- They both invest in the same local equity fund.

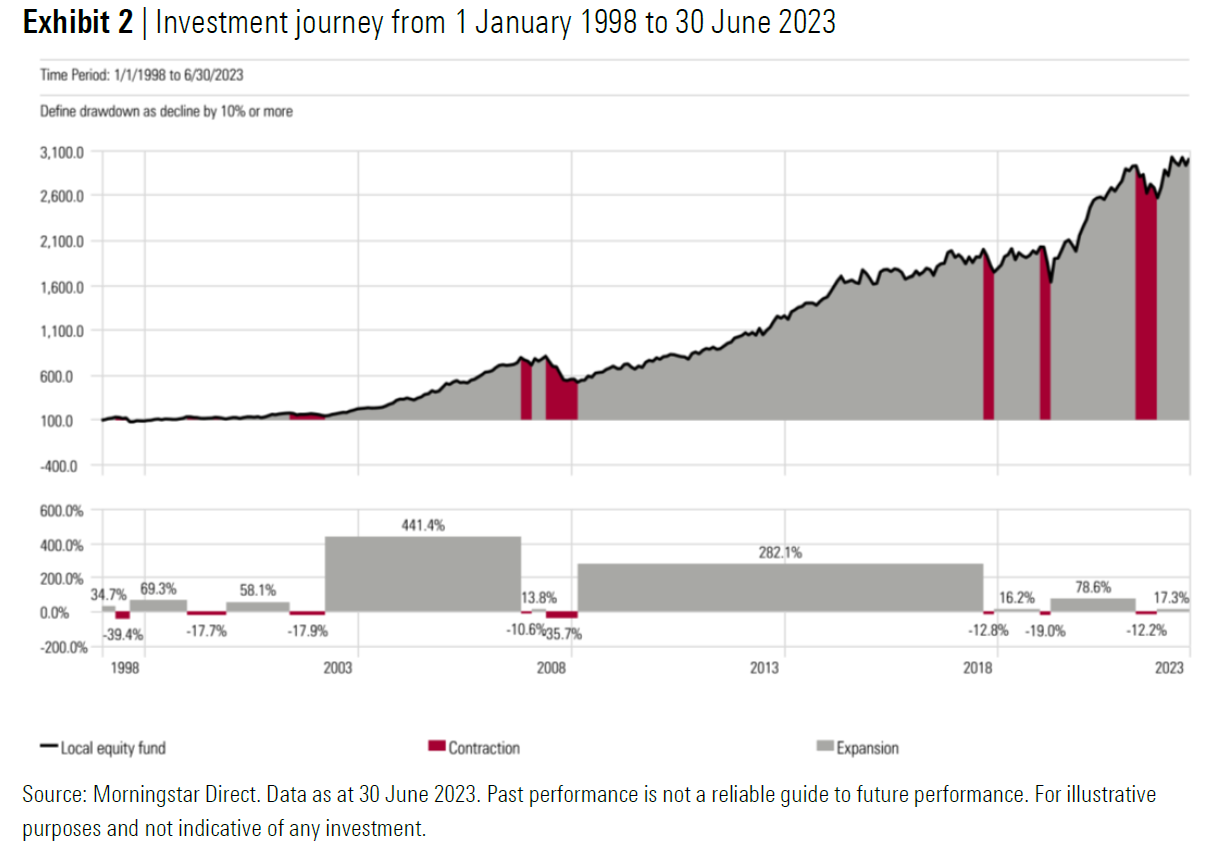

Below, we illustrate the journey of both of these investors. Over their 25-year investment journey, both investors experienced eight drawdowns of more than 10%. The worst drawdown, of close to 40%, occurred in 1998 just as they started their investment journey.

The big difference between the two investors is their investment strategies:

- After the first drawdown, Mr Market Timer moved his investment into a money market fund, only to get back into the market after market volatility subsided and the fund reached its previous peak. He continued to do this at every drawdown, disinvesting from the equity fund into a money market fund and buying back into the equity fund when volatility subsided.

- Mr Buy and Hold invested his capital into the local equity fund on the 1st of January 1998 and simply remained invested.

It is astonishing when we consider the difference between these two investment journeys –

- Mr Market Timer ended up missing the best days/months by deciding to withdraw and seek safety after a big drawdown in the market, costing him dearly when we look at his ending value in the below chart. This also acts as a good reminder that often the best days come after the worst in markets.

- It would have served Mr Market Timer better to just put his money in the money market fund and remain invested, rather than trying to time the market and switching out of the local equity fund to cash when he experienced a drawdown. With this said, being invested in cash over your investment journey would be a sure way to not keep up with inflation which can be detrimental to reaching your retirement goals.

- Mr Buy and Hold let compound interest work in his favour and ended with just over R14 million while Mr Market Timer ended with just over R3.6 million.

Mind the Gap

The persistent gap between the returns investors actually experience and reported total returns makes cash flow timing one of the most significant factors—along with investment costs and tax efficiency—that can influence an investor’s end results. In Morningstar’s Mind the Gap study, we dig into these nuances and explore how differences in the timing of cash flows, sequence of returns, and asset size can impact this gap.

The report found that fund investors earned a 9.3% investor return (which reflects the impact of cash inflows and outflows on the returns investors actually earn) over the 10 years ended 31 December 2021, while their fund holdings generated an 11.0% annual total return over the same period. Therefore, investors suffered a 1.7% annual return shortfall, or gap, due to mistimed purchases and sales. This annual return gap is in line with the gaps we measured over the four previous rolling 10-year periods, which ranged from 1.6% to 1.8% per year. Assuming compound interest, this is close to a 2% difference annually and can make a very large impact on your investment journey.

“The other 1% will change your life”

Hounsel’s quote goes on to say the above, implying that “most of what matters as a long-term investor is how you behave during the 1% of the time everyone else is losing their cool.”

It can be as simple as doing nothing. Buying and holding. Letting compound interest work its magic and your returns grow with time. Remember –

- Define your goals and develop a plan together with your financial adviser to achieve them.

- Save. You can’t invest money until you’ve saved money. Start as early as possible, a little bit can go a long way – remember compound interest is the eighth wonder of the world.

- Keep it simple. Don’t stray from your circle of competence. It’s all too easy to be lured outside your wheelhouse by friends, neighbours, or marketers. Complexity is costly and rarely yields benefits.

- Investing is a long-term pursuit – it’s not, and shouldn’t feel like a trip to Vegas.

- Time in the market, remains superior to timing the market.