Reap the maximum benefit from your Tax-Free Savings Account

With these essential tips

Abigail Wilson, CFP® Business Development Manager, Morningstar Investment Management South Africa

In 2015, National Treasury did us a solid with the introduction of Tax-Free Savings Accounts (TFSAs) in an effort to improve the overall savings rate of South African citizens. This is an incredible gift if used to its maximum – just picture how powerful the compound effect of tax-free returns can be over the long term.

How does a Tax-Free Savings Account work?

Before we delve into some key tips to reap the maximum benefit from your TFSA, let’s first remind ourselves of the salient features of the TFSA product:

- A Tax-Free Savings Account allows an individual to invest up to R500 000 over their lifetime into various asset classes without having to pay income tax, dividends tax or capital gains tax on the returns from the investment.

- It’s important to note that apart from the lifetime contribution limit of R500 000, there is also an annual contribution limit, which at the time of writing is R36 000 per tax year.

- The annual and lifetime contributions limits are aggregated across all TFSAs that an investor holds, so although an investor can have multiple TFSAs, it is essential that the total of the contributions to all of their TFSAs does not exceed R36 000 per tax year and R500 000 in their lifetime. Any contributions in excess of the limits will be penalised and taxed at a rate of 40%.

How can I maximise the benefits of my Tax-Free Savings Account?

Tip #1: View it as a long-term investment

It is unfortunate that “savings account” is included in the name of the TFSA product, as most individuals would associate this with something that is short-term in nature and use it to fund unexpected expenses. In the ideal world, we would rename it “Tax-Free Investment Account” – the word “investment” implying a nest egg left to grow for the long term. That said, there is no limit to the number of years you can let your TFSA grow and compound, and at Morningstar, we view the TFSA as a long-term vehicle, as the real magic – which is the compound effect of the tax saving – is only felt after extended periods of time.

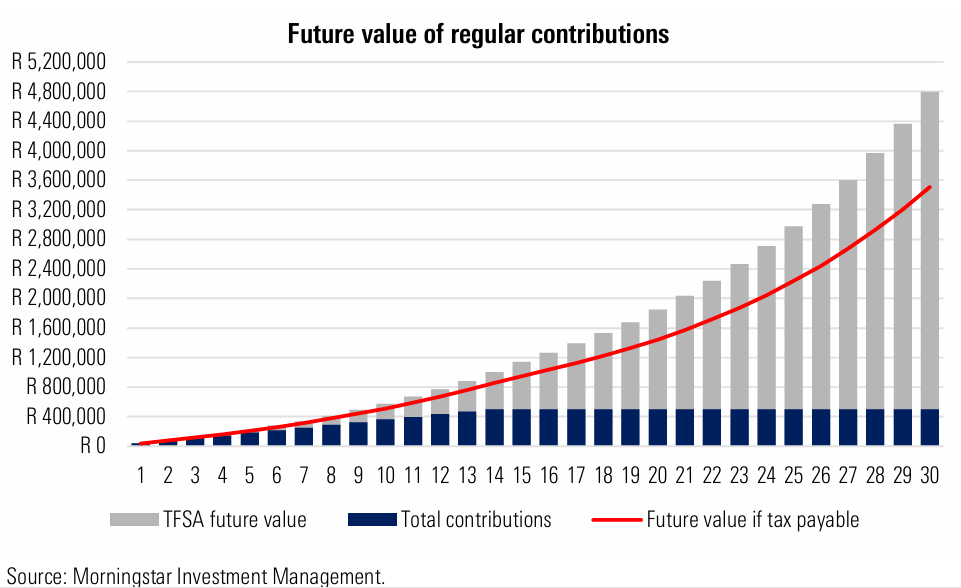

The tax benefit accrued from investing in a TFSA is highly dependent on an individual’s income tax bracket and the cadence of their contributions, however, it is worth looking at a real life example. This is illustrated in the following chart, which compares the returns generated over time from a TFSA versus a normal (taxable) unit trust.

The chart is based on the following assumptions:

- Annual contribution (at the end of each year): R 36 000

- Total contributions (achieved after 14 years): R 500 000

- Effective tax rate on returns (combination of income and capital gains): 30%

- Annual return: 10%

Looking at the above chart, we can see that in the short term, the effect of the tax saving is not very significant, however from about year 15 onward, the return differential between a TFSA and a normal taxable unit trust starts to widen; from year 20 it starts looking pretty decent, and over a period of 30 years, the cumulative difference in returns is substantial. After 30 years, the TFSA in this example grows to a value of close to R4,8 million, whereas the normal unit trust that was taxed, ends with a value of just over R3,5 million. And who doesn’t want an extra R1,3 million – that’s a pretty awesome gift from the government.

The lesson here? If you have an investment goal of less than 15 years, perhaps consider using a different vehicle for this goal such as a normal taxable unit trust or endowment (consult with your Financial Adviser to determine the best fit for you), rather than wasting your TFSA benefit on a short-term goal. The TFSA vehicle is most beneficial when it’s allowed to compound for 15+ years (ideally 30!).

Tip #2: Start early

Although there’s a limit to the amount you may contribute to a TFSA, there’s no limit to the number of years you can leave this sum to compound in value, earning tax-free growth. The earlier you start contributing, the sooner you can fill up your TFSA pot, and the harder that R500,000 will work for you. If you invest the R36 000 maximum contribution each year, it will take 14 years to reach the R500 000 lifetime contribution limit, and thereafter you want to leave the investment for as long as you can to really let the gap (as shown in the chart) widen. This makes the TFSA an ideal discretionary supplement to your retirement savings.

If your budget does not permit the maximum contribution, a lower contribution is still better than delaying contributions completely (due to the power of compound interest). Essentially, contribute what you can, as soon as you can – budget permitting, and keeping the rest of your financial needs and goals in mind.

Apart from starting at an early age, if you start early on in each tax year, it can also make a difference. If you have the financial means to contribute a R36 000 lump sum at the beginning of each tax year – you are giving this sum a 12 month head start on earning compound interest. However, it does require discipline to repeat this exercise on an annual basis. Another option is to implement a regular debit order of R3 000 per month – which will help you to ensure the consistency of your contributions. This is still more effective than contributing your lump sum at the end of the tax year.

Tip #3: Make alternative arrangements for a rainy day – and be careful – it’s liquid!

Don’t be fooled by the liquidity that a TFSA offers. Even though the product allows practically immediate access, you don’t want to use it as your emergency fund. TFSA product rules stipulate no minimum investment term, so no restrictions on access apply. This means you can request partial or full withdrawals at any age, and these withdrawals will be tax-free. However, this does not mean that withdrawing is without consequences, as with any contribution that you subsequently withdraw, you forfeit your right to re-contribute, as illustrated in the following examples:

Example 1: You have been contributing to a TFSA for several years, and thus far your contributions amount to R200 000. With growth, the full investment is currently worth R285 000. You withdraw the full investment value of R285 000. If you decide to start contributing to a TFSA again, you will only have R300 000 remaining of your lifetime limit (R500 000 lifetime limit minus R200 000 prior contributions = R300 000 lifetime contributions remaining). The R85 000 that was derived from investment growth will not reduce your lifetime limit.

Example 2: If you contribute R36 000 (the maximum) at the beginning of the tax year, and you withdraw R20 000 later on in the same tax year, you may not re-contribute R20 000 back to a TFSA during the same tax year. If you do re-contribute R20 000, SARS will calculate your annual contributions as R56 000 (R36 000 initial contribution + R20 000 re-contribution), which is R20 000 in excess of the R36 000 annual limit, and the R20 000 excess will be penalised with 40% tax payable to SARS (R 20 000 x 40% = R 8000 penalty).

The lesson here? Avoid dipping into your TFSA early. Speak to your financial adviser to ensure that you have a different account to provide adequate funding for emergencies or shorter-term savings goals.

Tip #4: Have sufficient exposure to growth assets

While risk tolerance is a key factor to consider when selecting the appropriate asset classes for your investment, so too is time horizon. If you are maximising your TFSA by giving it a 15 year+ time horizon to grow, you’re going to gain the most benefit from having significant allocations to growth assets such as equities. This is based on the long-term outperformance of equities versus more conservative allocations such as cash and fixed income.

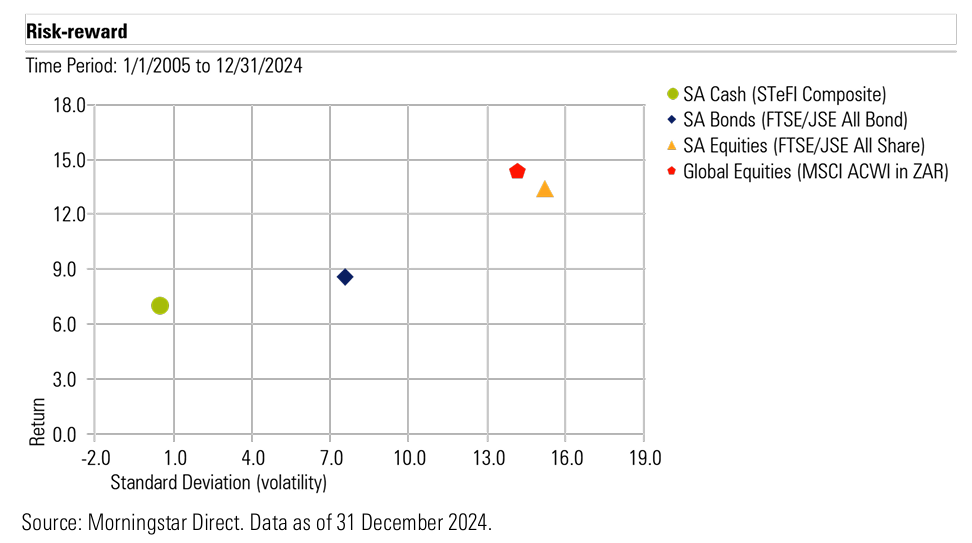

The below chart plots the annualised return (y-axis) and the volatility as measured by standard deviation (x-axis) for SA Cash, SA Bonds, SA Equities and Global Equities, over 20 years. Although they have higher levels of volatility, with sufficient time on their side, the highest returns were achieved by the growth assets (Global Equities and SA Equities).

Another great benefit of the TFSA product is that it’s not subject to any regulatory limits in terms of asset allocation, and therefore does not limit the amount that can be invested in equities or the amount that can be invested in offshore asset classes. This contrasts with Retirement Annuities, Pension Funds and Provident Funds which are restricted to a maximum of 45% offshore asset exposure due to Regulation 28 of the Pension Funds Act. A TFSA, therefore, allows an individual to diversify away from South African specific risks through a highly tax-efficient product.

In summary

The benefits of a Tax-Free Savings Account make it a no-brainer, but importantly, speak to your Financial Adviser to ensure that you are using your TFSA for the right purpose, and to help you select a suitable investment portfolio to deliver on your return objectives.

This commentary does not constitute investment, legal, tax or other advice and is supplied for information purposes only. Past performance is not a guide to future returns. The value of investments may go down as well as up and an investor may not get back the amount invested. Reference to any specific security is not a recommendation to buy or sell that security. The information, data, analyses, and opinions presented herein are provided as of the date written and are subject to change without notice. Every effort has been made to ensure the accuracy of the information provided, but Morningstar Investment Management South Africa (Pty) Ltd makes no warranty, express or implied regarding such information. The information presented herein will be deemed to be superseded by any subsequent versions of this commentary. Except as otherwise required by law, Morningstar Investment Management South Africa (Pty) Ltd shall not be responsible for any trading decisions, damages or losses resulting from, or related to, the information, data, analyses or opinions or their use. This document may contain certain forward-looking statements. We use words such as “expects”, “anticipates”, “believes”, “estimates”, “forecasts”, and similar expressions to identify forward-looking statements. Such forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results to differ materially and/or substantially from any future results, performance or achievements expressed or implied by those projected in the forward-looking statements for any reason. Morningstar Investment Management South Africa Disclosure The Morningstar Investment Management group comprises Morningstar Inc.’s registered entities worldwide, including South Africa. Morningstar Investment Management South Africa (Pty) Ltd is an authorised financial services provider (FSP 45679) regulated by the Financial Sector Conduct Authority and is the entity providing the advisory/discretionary management services.